The Shrinking Dollar

As we move to a non-cash, electronic payment economy, the perception of the value of money is changing. I remember in my last years of college when $1 would buy a gallon of gas and a pack of cigarettes or a Big Mac and I would still receive change back from my buck.

That was a time when a single, physical dollar bill carried real weight in American life. Today, that same $1 bill still looks official, still bears the familiar portrait of George Washington and still qualifies as legal tender for all debts public and private. But its practical buying power has radically changed.

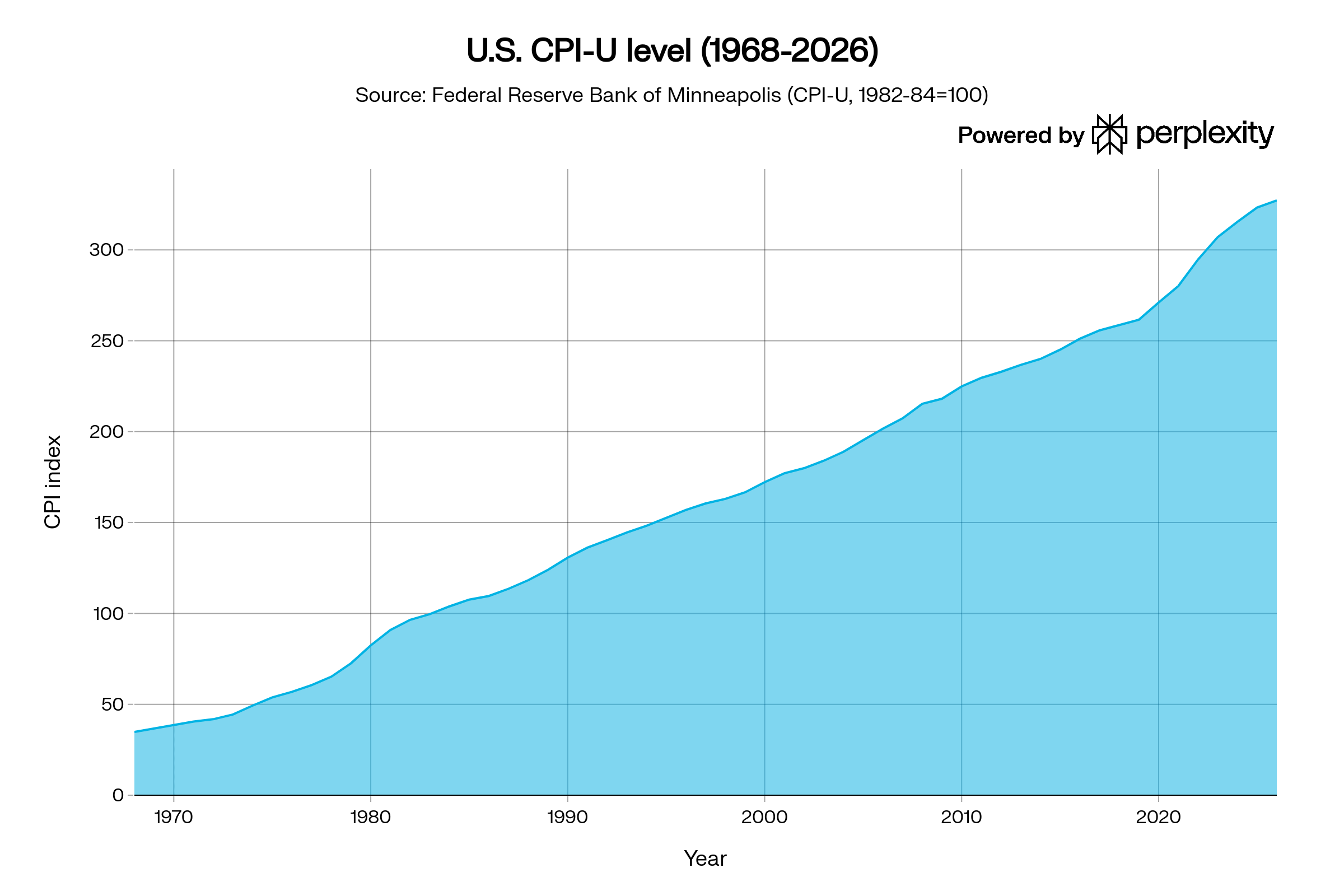

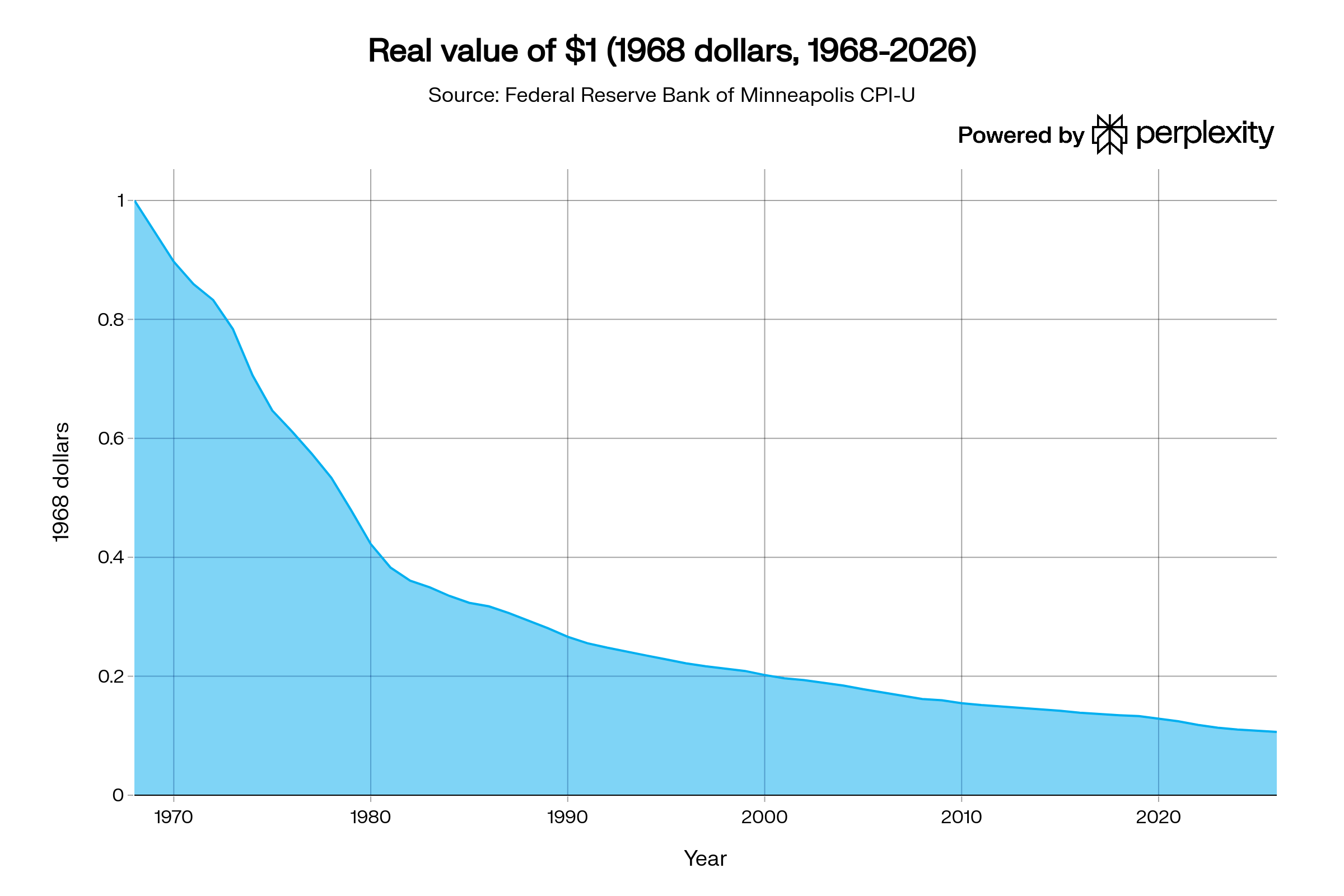

Measured against the steady rise in prices over time, that same dollar, according to the U.S. Consumer Price Index, now buys only a fraction of what it once did. In real terms, the dollar’s purchasing power has fallen to about 9.6 cents which means that about 90 percent of its value has gone up in smoke.

I almost never think about this crushing metamorphosis because today the financial system runs on credit and debit cards where the exact amount is charged. You never get change back from your dollar because you are no longer paying in cash. There is no math needed with purchases made with a tap of your credit card.

As a baby boomer, I must ask, “How did this happen?” and “Where did my money go?”

The answer is obvious ... inflation.

What That Really Means

Inflation does not destroy money overnight. It works slowly, quietly and relentlessly. Prices rise year after year, often by amounts small enough that people barely notice. But over decades, the effect becomes enormous and few of us are really keeping track of it.

If today’s dollar is worth only about 9.6 cents in relative purchasing power to my 1968 dollar, what happened? The answer is: my dollar did not disappear entirely. It was just diluted by forces out of my control.

That is why older Americans often speak about the prices of the past. Coffee for a dime. New cars under $3,000. Homes in working-class neighborhoods for under $25,000. Those numbers sound mythical today.

The Tale of the Tape: Consumer Price Index (UP) vs. Real Value of $1 (Down)

How It Happened

The principal reason is cumulative inflation. Since the creation of the Federal Reserve System in 1913, the United States has experienced wars, recessions, booms, oil shocks, pandemics, asset bubbles and massive expansions of government spending. Each era left its mark on prices.

During wartime, governments borrow and spend heavily. During recessions, central banks often lower rates and expand liquidity. During growth periods, rising wages and demand can push prices higher. Over time, these cycles compound.

No single president or central banker caused the decline alone. It is the accumulated result of more than a century of monetary management, political decisions, debt expansion and economic shocks.

Silent Forces at Work

Inflation has repeatedly forced American policymakers, especially the Federal Reserve System, to raise interest rates, often with the unintended consequence of slowing the economy sharply enough to trigger recessions. The pattern is consistent: prices accelerate, credit becomes too easy and the central bank responds by tightening money. That tightening curbs borrowing, spending and investment and, if pushed far enough, it breaks economic momentum.

One of the earliest and most severe examples came after World War I. Inflation surged as wartime demand unwound and speculation took hold. In response, the Federal Reserve raised rates aggressively in 1919-1920. The result was the brutal recession of 1920-1921, one of the sharpest contractions in American history. Prices collapsed, unemployment spiked and businesses failed in large numbers. It was a stark demonstration that rapid tightening, while effective against inflation, can choke off economic activity with surprising speed.

A more complex version of this dynamic unfolded during the lead-up to the Great Depression. While the 1920s were marked by growth, underlying imbalances and periods of monetary tightening helped restrict liquidity. When the system finally broke in 1929, the downturn deepened into a full depression. Although the causes were broader than inflation alone, the lesson endured: shifts in monetary policy can amplify economic vulnerability at critical moments.

The most famous modern example came in the late 1970s and early 1980s, when inflation spiraled into double digits. Under Fed Chairman Paul Volcker, the central bank pushed interest rates to extraordinary levels, at one point exceeding 20 percent, to break inflation’s grip. The cure worked, but at a cost: the U.S. economy fell into back-to-back recessions in 1980 and 1981-1982. Unemployment rose above 10 percent, businesses struggled and entire sectors, particularly housing and manufacturing, contracted sharply.

Even in more recent decades, the same mechanism has appeared in milder form. Periods of rising inflation, such as in the late 1980s, early 2000s, and again after the pandemic-era surge, have led to tighter monetary policy. Each time, higher interest rates slowed borrowing, cooled housing markets and reduced consumer spending. While not always resulting in deep recessions, the risk has remained constant: when inflation forces rates higher, economic growth becomes fragile.

The historical record is clear. Inflation does not simply erode purchasing power, it compels action. And when that action takes the form of sharply higher interest rates, the economy often pays the price.

The Hidden Tax

Inflation is often called a hidden tax because it reduces what savings can buy. A person who stores cash for decades without earning returns may discover that the money remains numerically intact but economically weakened. Inflation is the silent thief in the night that steals from the rich and the poor, but the poor feel the pain much, much more

Someone who saved $10,000 in cash many years ago might still have $10,000 today, but that money may purchase only a small portion of what it once could. This is why investors turn to stocks, real estate, bonds, businesses and commodities: they seek assets that can outrun currency depreciation. To buy what you could in 1968 with $10,000 would take about $96,000 today.

Why It Matters in 2026

In 2026, Americans feel this reality every day. Grocery bills, rent, insurance, medical care, tuition and home prices have all risen dramatically relative to past generations. Wages may be higher in nominal terms, but many households feel squeezed because dollars stretch less than they once did.

That creates social tension. Workers demand raises. Retirees worry about fixed incomes. Younger families struggle to buy homes. Savers resent low returns when prices rise faster than interest earned.

The debate then becomes political: should the nation prioritize growth, debt reduction, stable prices, stronger wages or easier money? Each path has winners and losers.

The Symbol of the Dollar

The irony is that the dollar remains one of the strongest and most trusted currencies in the world. It is still the backbone of global trade, reserve holdings and financial markets. Yet even a dominant currency can lose domestic purchasing power over time.

That is the lesson of the modern $1 bill. It still commands respect abroad, but at home it buys less each year unless inflation is contained.

A $1 Federal Reserve Note may still say “one dollar,” but labels can mislead. If it’s real value has fallen to 9.6 cents in purchasing power terms, then the story is not about paper money, it is about time, policy and the silent mathematics of inflation. The dollar value did not implode in a dramatic crash. It faded slowly away, year by year, in plain sight.

To rest comfortably as the relentless assault of inflation devalues your purchasing power is to fail to pay attention. When confidence in America and its ability to handle its finances erodes and when the cost of carrying the national debt squeezes out the private credit market or forces higher taxes or reduction in social services, the bill for decades of kicking the can down the road could come due ... all at once.

My column sees the world through the lens of Americana and focuses primarily on the history and culture of the United States. It uses the latest technological innovations combined with over seven decades of personal experience to create a vehicle that helps to communicate issues that have resonated throughout the history of the American experiment. My column is free to all.